As volatility roils the commodity markets, corporations face difficult decisions in managing financial risk. For many, achieving long-term success requires dispelling misconceptions and facing uncomfortable truths about the commodity markets and their approach to managing exposures. This article outlines five “lies” corporates tell themselves about commodity markets and offers recommendations for moving forward with leading practices for managing commodity risk.

-

“We'll see it coming.”

Corporate finance teams commonly believe deep industry experience and immersion in the current markets will enable them to detect early signs of market disruption. In reality, though, no one can foresee the next black swan event.

Unforeseen issues ranging from geopolitical upheaval, evolving trade agreements, tariffs, and sanctions to natural disasters and extreme weather events can disrupt commodity markets. If the major oil companies – with perfect visibility into their drilling and production plans, tanker charters and loadings, and refinery turnaround schedules – can’t predict or control the fuel markets, what makes us think that we can see and predict what BP or Shell can’t?

Similarly, it’s impossible to foresee where weather or war will disrupt agricultural planting and harvesting seasons.

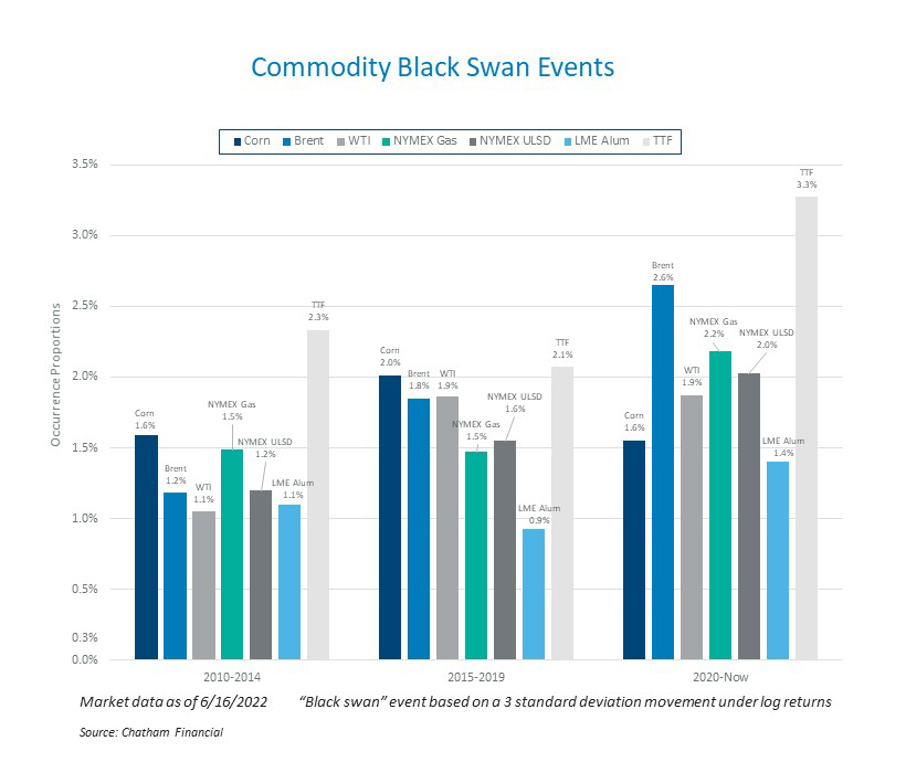

While we don’t know what will cause the next market explosion, we can be sure one is on the horizon. Black swans, “once in a lifetime” events that totally disrupt markets, happen more than you think. Statistics suggest that they should happen only three out of every 1,000 occasions, but they have occurred seven times more frequently than expected in volatile commodities.

The good news is that corporates can still prepare for shifting market cycles by developing clear-cut hedging objectives that are actionable and measurable.

Your goal shouldn’t be to eliminate all the risk. Rather, aim to take the big roller coaster and make it small, reducing the peaks and valleys on financial statements so you have time to adjust your business model. If it takes 18 months to revise your pricing or make operational changes, having hedges in place to minimize disruption buys time for your organization to adjust.

The bottom line: Don’t always make commodity risk management the last thing you get to. When the swings come, they’re sharp, fast, and often unpredictable.

-

“We don’t speculate; we just hedge opportunistically.”

Many corporate risk management policies preclude market speculation while including language that allows for opportunistic hedging. While it feels great to get in the market at the right time, attempting to time the market can put your organization at risk. In the same way, choosing not to hedge because you don’t like the current price is speculation; you’re taking a position based on where you think the market will go.

It’s important to differentiate between opportunistic hedging and speculation. The reason you hedge is to reduce risk by narrowing the range of potential outcomes. Conversely, speculation involves taking on risk to benefit from changes in market pricing.

In 2014, for example, Brent had mostly been in the $100-to-$120/Bbl range for three years. It then started to collapse and fell to $60/Bbl. Opportunistic hedgers, anticipating a quick rebound to higher prices, jumped in and bought a multitude of hedges before analyzing the root cause of the market collapse.

When the market continued to fall, dropping another $25, and finally bottomed in the $35/Bbl range, many companies found themselves with outsized hedge books at extremely unfavorable prices. Many airlines found themselves in this position with limited credit capacity under their credit support annexes (CSAs) and unable to add additional barrels at multi-year lows. Ironically, many of the same airlines, that were paying out monthly on unfavorable hedges, suspended their programs and were caught unhedged when the market rebounded in 2017.

Avoiding speculation doesn’t mean you can’t take advantage of market opportunities. You just need to put guardrails in place to ensure the hedge aligns with your strategic objectives.

If you have a target budget and the market falls well below it, increasing your hedge ratio and taking on additional coverage can be beneficial. However, you then need to be prepared for a scenario where the market continues to fall. The key is to identify and quantify your exposures so that all stakeholders – the financial team, the procurement team, the senior management team and others – understand the value of risk reduction and are prepared to absorb the costs of unfavorable hedges. For example, procurement typically seeks year-over-year price reductions on commodities, so they may be inclined to hold an exposure rather than buying a commodity at a higher price. This can create hidden exposures.

The bottom line: Identifying your exposures and developing a hedging strategy in advance can provide the flexibility to take advantage of market movements without veering into speculative territory.

- “The market is volatile, so we need to change our strategy.”

When commodity prices skyrocket, there is often pressure on financial teams to adopt new strategies. While hedging programs should be nimble and enable tactics that can flex with the changing market, your overall strategy should stay consistent if the objectives haven’t changed. To ensure your strategy can weather volatility while accommodating business changes and market dynamics, you need to differentiate between the underlying hedging strategy and the tactics that support it.

When you invest in the data, personnel and processes to implement a hedging program, you should also be prepared to measure the program’s results and determine whether they meet its objectives. These objectives should be based on the risk quantification of your portfolio including exposures and hedges, defined risk-tolerance levels, and priorities.

Bryant Lee is Chatham Financial’s head of commodities.

An example of this kind of metrics-based decision-making would be an objective to “keep the variance on our aluminum pricing below 15% over an 18-month horizon.” Then, underpinning that objective is a strategy such as, “We’re going to hedge using a mix of fixed-price physical with our vendors and financial derivatives with our banks.” These strategic elements should remain consistent despite different market environments with the flexibility to make changes at the tactical level, where you break down into each of the individual sub-commodities and determine hedging indices, instruments, tenors, and horizons.

The bottom line: If you change your strategy every time the markets swing back and forth, you end up chasing your tail and getting nowhere.

- “We can't achieve hedge accounting, so we shouldn't hedge.”

It can be challenging for a commodity risk management program to qualify for hedge accounting, and organizations are understandably concerned about how their hedges are impacting their financial statements. However, this doesn’t justify ignoring the risk, which can continue to increase and threaten your margins and profitability.

Rather than allowing risk to grow unchecked, you should analyze and quantify your exposure, decide whether the risk is meaningful, outline the potential operational and hedging strategies, and determine whether your planned approach can qualify for hedge accounting. Then, even if you decide hedging isn’t the correct course of action, you have quantified the risk and can point to metrics that support the decision.

For example, an organization is exposed to PVC. Despite PVC following the general resin price trend, there is very limited trading with virtually no visibility into the forward curve and prevailing market price, making it difficult to discern a reasonable and efficient execution price. They face this same issue when negotiating a fixed-price supply agreement with their supplier. If the risk is meaningful, the company could hedge in the short term to minimize the P/L noise or work with the supplier to see if the required feedstocks could be priced on a more liquid index.

The bottom line: If you assess a commodity exposure and determine it is a meaningful risk, you need to find a way to mitigate the accounting risk as well.

- “We can handle it ourselves.”

No matter how knowledgeable, experienced and well-staffed your financial team is, collaboration and strategic alignment, both inside and outside your organization, are critical for capturing and managing your financial risks. For commodities, internal alignment becomes more complex since procurement or supply chain management, rather than treasury, is often tasked with managing this risk.

Unlike the treasury team, which seeks earnings stability, the procurement team focuses on achieving year-over-year cost reductions. This can create financial risk when procurement faces higher pricing on the commodity and chooses to delay the purchase. However, the finance team may not even be aware of this exposure until the price escalates rapidly. By engaging with procurement, you can collectively determine whether managing risks with derivatives might provide more control and flexibility than purchase contracts or supplier agreements.

It’s also important to negotiate with commodity counterparties from a place of knowledge. Very few organizations are exposed to the exact “benchmark” commodity that trades. For example, if your organization is exposed to fuel prices at the pump, you may want to hedge using the DOE On Highway Diesel Index. To understand what price is fair to hedge your pump price versus the bank’s offer price, you need to know what index trades, who trades it well, understand basis risk, and perform a correlation analysis.

When you’re ready to execute a hedge, the person on the other end of the phone is dealing with diesel and gasoline all day long. Unlike in foreign currency, you can’t always look at a screen to see where the pricing is. Without that transparency and liquidity, leveraging a partner with subject matter expertise can level the playing field.

The bottom line: Collaboration and strategic alignment, both inside and outside your organization, are critical for capturing and managing your financial risks.

The next year will bring many opportunities for treasury teams to deliver value to their organizations. By understanding and avoiding these common pitfalls, you can take the lead in collaborating with internal and external stakeholders, outlining measurable hedging objectives, and developing the strategies and tactics to achieve a successful commodity risk management program.

Bryant Lee is a director on Chatham Financial’s Treasury Advisory team, where he advises clients on commodity risk with a primary focus on energy and base metals. Prior to joining Chatham, he founded and directed an energy risk management firm that helped Fortune 500 clients reduce energy expense, mitigate risk, and identify efficiency opportunities.

Topics: Financial Markets