In the digital age, where financial transactions have become the lifeblood of businesses, payment and transaction fraud have emerged as significant threats. Our recent Financial Security Trends survey of 659 finance executives in the U.S. has shed light on the alarming prevalence of payment fraud in organizations, along with the primary reasons, costs, and consequences.

The findings shed light on why payment fraud is on the rise, its financial implications, the after-effects on companies, as well as the measures companies are taking to mitigate these risks, and highlight the challenges they face in doing so.

The Alarming Statistics

More than 80% of respondents reported that their organizations experienced at least one payment transaction fraud in the past two years, and 51% had at least four incidents. These came at a substantial cost, with an average per-incident rate of $149,225. Shockingly, it took more than a month to over a year for 76% of respondents to discover and address the discrepancies.

Creednz CEO Johnny Deutsch

Several factors contribute to the growing risk of payment and transaction fraud:

- 59% of respondents cited the increasing sophistication of fraudsters as a primary reason behind the rise in payment fraud.

- 56% noted a lack of resources and technology systems to proactively identify Accounts Payable (AP) and Accounts Receivable (AR) fraud.

- 53% of respondents identified vulnerabilities in their business processes as a contributing factor.

Responsibility and Accountability Disconnect

Interestingly, IT security/SecOps (security operations) were identified as the most responsible for preventing fraud (34% of respondents). However, these departments often lack the necessary tools, resources, or knowledge to prevent fraud proactively. Finance/treasury departments, on the other hand, are held most accountable.

Many struggle to identify the root causes. The largest number of respondents cited internal fraudsters (45%) and external fraudsters (40%), but 36% said their organizations could not determine the root cause. Only 32% were confident that their banks would verify and stop suspicious transactions.

“These findings emphasize the importance of implementing effective fraud detection and prevention measures to minimize the impact of transaction fraud and reduce the time it takes to discover it,” the report says.

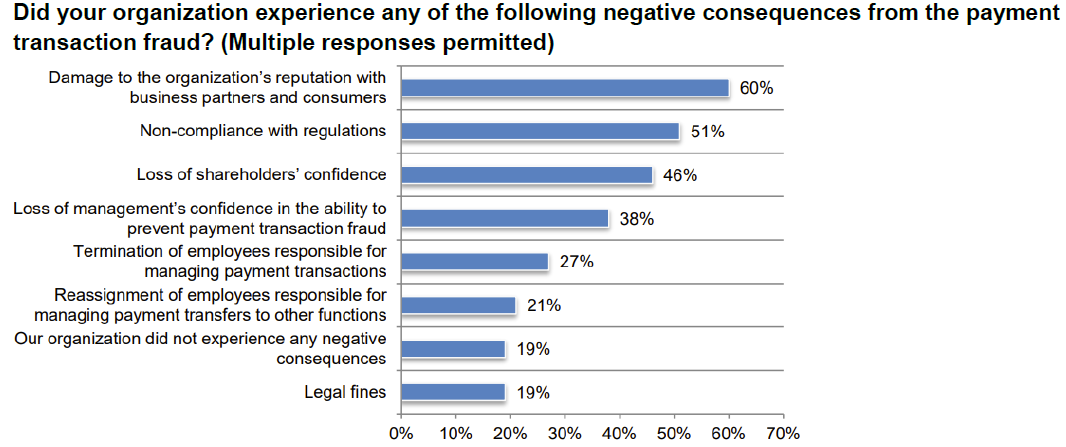

The Real Cost of Payment Fraud

Aside from the financial cost, payment fraud incidents inflict other severe consequences. The most significant among them is reputational damage, cited by 60% of respondents. This is followed by non-compliance with regulations (51% of respondents) and loss of shareholders' confidence (46%).

Source: Financial Security Trends ’23

In addition, the globalization of business has brought new challenges. Almost half (48%) of respondents have bank accounts outside the U.S. and Canada. With accounts spread across regions like EMEA, LatAm and Asia-Pacific, the complexity of managing cross-border transactions has increased.

Fraud concerns are particularly acute when making payments to third parties and vendors outside the U.S. and Canada. A majority of respondents expressed concerns when dealing with overseas organizations, with varying levels of worry across regions.

Mitigation Steps

In response to payment fraud incidents, organizations have taken several steps to minimize future risks. The most common measures include:

- Bank account access privileges, which 69% of respondents use to minimize payment fraud.

- Daily review and approvals, conducted by 64% on all outgoing payment transactions.

- 61% have added ACH (automated clearing house) blocks or filters.

- Multi-factor authentication, implemented by 60%.

The findings underscore the urgent need for organizations to prioritize payment and transaction fraud prevention. As fraudsters become more sophisticated, organizations must invest in technology, resources and robust processes to proactively identify and address vulnerabilities. With the financial and reputational stakes so high, organizations cannot afford to be complacent.

Johnny Deutsch is CEO and co-founder of Creednz, which enables finance teams to make informed and protected B2B payments in real time. The former CISO at Rivian Automotive and two more publicly traded companies, Deutsch led EY’s offensive cybersecurity services for a decade and served seven years as the Deputy CISO for the Israeli Ministry of Defense elite unit.

Topics: Counterparty