Bigger is better. At least, it seems, with respect to the riskiness of banks.

The capital, profitability and credit risk differences between small and large banks were highlighted in a European Bank Authority (EBA) report that included end-of-year 2020 data. Interestingly, the data showed that over the 2018 - 2020 time period, small banks actually had higher return-on-equity (R0E) than their larger brethren, but also took more risk (at a greater cost), required larger capitalization (to support riskier assets) and tended to invest in higher-risk portfolios.

Not surprisingly, the numbers were somewhat skewed by the economic impact of the COVID-19 pandemic in 2020. While loans under EBA-eligible moratoria showed normalization (nearly halving in Q4), profitability remained “subdued.”

Size-Based Disparities

The EBA's risk dashboard measured the performance of banks across a host of parameters (including ROE, CET1 and net interest margin), and predicted that strong competition will continue to add pressure on bank margins. Through this dashboard, the EBA also presented outcomes for small banks and large banks separately - per parameter, per quarter.

Size classification was based on a bank's average total assets between December 2014 and December 2020. The “small banks” were described as those with assets below the first quartile (see footnote on page 3 of the risk dashboard report), while “large banks” were depicted as those with assets above the third quartile.

Small banks have different risk profiles, profitability, and capitalization than large banks. This is apparent in the “standardized difference for small banks”- a risk measurement tool in which we calculate the percentage difference of a given parameter (e.g., ROE) between small and large banks, and then divide that number by the value for large banks.

For example, in the EBA's report, for 2020, the ROE parameter is equal to 6.88% for small banks and 2.06% for large banks. The standardized difference for this parameter can therefore be simply calculated as follows:

The results of this standardized difference calculation are presented (per measurement parameter, per year, for the past three years) in the chart below.

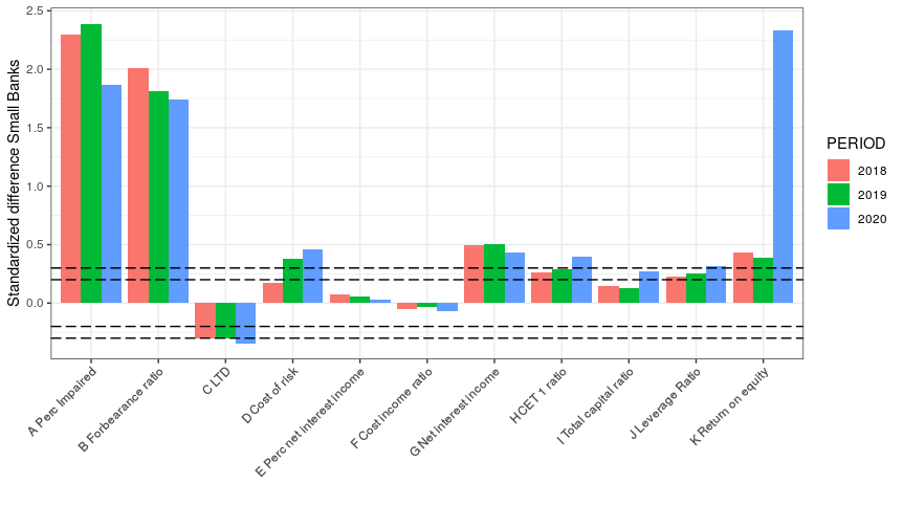

Standardized Differences for Small Banks - Per Parameter, Per Year

To highlight significant differences between large and small banks, we have selected specific EBA parameters (from A to K), and added thresholds at the +/-20% and +/- 30% levels.

The first result we see is that, per euro exposure, small banks take more risk than large banks, on average. Indeed, the impaired and forborne percentages (parameters A and B) at small banks are significantly higher than for large banks.

As a result, small banks' loan-to-deposit ratio tends to be lower (see parameter C). While their cost of risk (see parameter D) is higher, the difference is not as significant as we see for parameters A and B. Moreover, the higher costs of risk borne by small banks are compensated by higher income (see parameter G).

Since they need more capital to support their riskier assets, capital ratios also tend to be higher for small banks. This applies not only to CET1 ratio but also to total capital and leverage ratios (see parameters H, I and J). However, the difference between capital ratios at large and small banks is not as pronounced as the riskiness gap, which is line with our observation for cost of risk.

Interestingly, from the perspective of ROE, small European banks have performed significantly better than large banks during the past three years. Indeed, as expressed in the capital that is needed to support the business, smaller banks tend to generate higher interest income.

Last year, amid the COVID-19 pandemic, this tendency was even more pronounced, because small differences between ROE levels were inflated by the standardization - or the low denominator value of the standardized difference.

Of course, the higher ROE at small banks comes at a risk for investors. In their hunt for yield in this low interest rate environment, small banks may invest more heavily in high-risk portfolios; if the underlying systematic drivers of these portfolios develop unfavorably, the consequences of this type of approach can be severe.

In the U.S., for example, small banks have higher exposures in commercial real estate (CRE) portfolios, and have suffered as a direct result of the pandemic-driven price drop in CREs. “The impact of a decline in CRE prices is especially true for small and community banks, which tend to have the highest CRE loan exposures,” the International Monetary Fund noted in its May report on CRE trends.

Parting Thoughts

The EBA's risk dashboard helped to identify 2020 trends but also was able to provide a broader, in-depth, three-year breakdown of the risk profile, capital ratio and profitability differences across small and large EU banks.

Marco Folpmers

Last year, in response to economic hardships driven by the pandemic, banks were given government protection that shielded them from potentially outlandish credit risk. Theoretically, this may have created a moral hazard, since small banks were able to maintain a higher interest rate margin while having at least part of their risk exposure temporarily covered by government-support packages.

Generally speaking, small banks have riskier portfolios (particularly across the past few years) - but they seem to be able to amply compensate for the cost of risk with the help of a higher interest margin. The question, however, is whether the higher ROE levels small banks have experienced are sustainable long-term, given the inherent systematic risk these banks incur.

Dr. Marco Folpmers (FRM) is a partner for Financial Risk Management at Deloitte Netherlands and a professor of financial risk management at Tilburg University/TIAS.