Faster payment initiatives in the U.S. are catching up to and could surpass networks that got an earlier start in other countries. The Federal Reserve's pending FedNow Service promises to widen the range of choices in the marketplace.

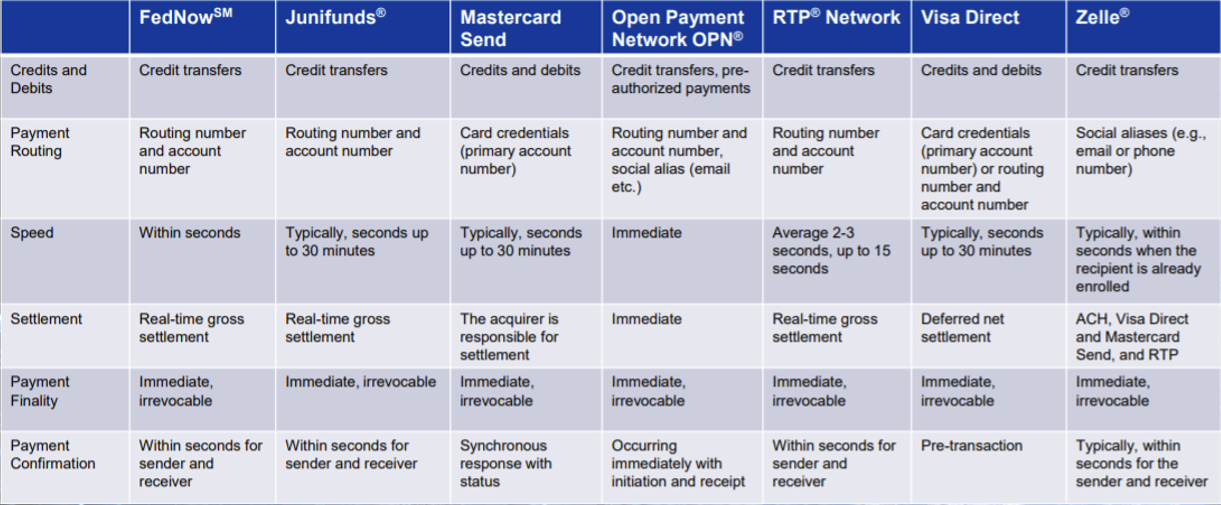

FedNow is about two years in development, with proposed rules for the service currently open for public comment. Meanwhile, The Clearing House (TCH) RTP real-time payments network, which began testing in 2016, has gone national. It reached 120 banks and 60% of demand deposit accounts as of May, enabling real-time settlement of payments up to $100,000.

The National Automated Clearing House Association, which has historically handled electronic payments in periodic batches, introduced same-day settlement in 2016 and added a third same-day submission window in March. The ACHs extended the window for same-day payments to 4:45 pm ET, in addition to overnight settlement, and in March 2022 will increase its payment maximum to $1 million, from the current $100,000.

“Consumers and businesses across the country want and expect instant payments, and the banks they trust should be able to provide this service securely,” Fed governor Lael Brainard said in an August 2020 webinar, mentioning credit risk mitigation as a key benefit of real-time transaction settlements.

Digital Economy and Currency

These efforts followed the lead of the Federal Reserve's multi-stakeholder Faster Payments Task Force, which convened in 2015 to consider payment-system modernization in the light of an increasingly digital economy.

On a separate track, the Fed has followed many of its central banking peers in exploration of potential central bank digital currencies (CBDCs) employing blockchain technology. The Fed plans to issue a discussion paper on the subject this summer, chair Jerome Powell said in May.

Along with efficiencies, policymakers see advanced payments as a social, financial inclusion benefit. Speaking in May, Brainard said, “CBDC may be one part of a broader solution to the challenge of achieving ubiquitous account access. Depending on the design, CBDC may have the ability to lower transaction costs and increase access to digital payments.” For emergencies, such as in delivering stimulus funds during the pandemic, “CBDC may offer a mechanism for the swift and direct transfer of funds, providing rapid relief to those most in need.”

A CBDC provision was proposed, but ultimately not included, in a U.S. stimulus bill last year.

Former Commodity Futures Trading Commission chairman J. Christopher Giancarlo, in June 9 Senate Banking subcommittee testimony on behalf of the Digital Dollar Project, said, “Had a digital dollar been in circulation during the COVID-19 crisis with a means of digital identification, it would have enabled the immediate sending of monetary relief to the digital wallets of targeted beneficiaries.

“During non-crisis conditions,” Giancarlo added, “a digital dollar could be a useful tool in the distribution of other government assistance payments, such as Social Security benefits, school meal vouchers and food stamps, among others. It may also serve to expand financial inclusion for underserved populations due to lower system costs and the ready availability of digital wallets.”

A week later, in advance of a House Financial Services Committee financial technology task force hearing, Bank Policy Institute president and CEO Greg Baer was more cautionary: “The push for CBDCs is oddly timed given the revolution in real-time payments that is already underway, and its proponents ignore or minimize the reduction in lending and economic growth that would come if consumers and businesses could instantly move their money from bank deposits into a digital mattress. Major policy problems remain to be solved.”

Gradual Adjustments

U.S. faster payment initiatives were slow to take off, said senior Aite Group analyst Erika Baumann, because unlike in most countries that already have real-time payments, there has been no federal mandate to switch. The U.S.'s large and decentralized banking system also complicates coordination efforts.

Despite the ACH network's ubiquity, even same-day payments took a while to catch on. They jumped 88% in the 2021 first quarter, year-over-year, to 141.1 million, and in terms of value rose 133%, to $187.6 billion.

ACH Network senior vice president Michael Herd said the surge came after market participants had taken time to ready their systems, and was probably linked to “heightened awareness” of upcoming enhancements.

“The ability to put a transaction into the ACH and know it's going to reach accounts where you need it to go is very powerful,” said Reed Luhtanen, executive director, U.S. Faster Payments Council. He pointed out that technological progress tends not to quickly displace older methods: Checks only recently dropped below 50% of business payments. The ACH, he added, “still has a lot of utility, particularly for bulk transactions scheduled regularly.”

Core-System Connections

TCH anticipates the number of banks using its RTP to accelerate, because core system vendors like Fiserv and Jack Henry have recently connected to its network and its features such as request for payment (RFP), which greatly reduces the risk of overdrafts.

The Federal Reserve participated in the RTP vetting process, Baumann said, and its later decision to pursue FedNow, which could launch by 2023, disrupted the payments market. Some banks that planned to go live with RTP instead paused, she said, but that number has likely declined given the opportunity cost of not moving ahead sooner with real-time payments.

PNC Bank, part of PNC Financial Services Group, the fifth-largest U.S. commercial banking organization including the recently acquired BBVA USA, joined in a June 15 announcement with TCH and DailyPay to deliver earned income to workers instantly via RTP. It's positioned as a cheap and efficient alternative to payday loans.

“Paying workers on demand has taken on a new level of importance during the ongoing pandemic and helps to address cash flow concerns that many workers face on a weekly basis,” said TCH senior vice president of product strategy and development Steve Ledford. “DailyPay's utilization of the RTP network provides a seamless user experience and benefits the worker and the employer.”

Some regional and community banks were said to be wary of joining RTP because of TCH's big-bank ownership. The Fed's Brainard addressed the access issue last year: “Our public mission in providing payment services is built on the proposition that all banks and the communities they serve, no matter their size or geographic location, should have equitable access to the U.S. payment system.

“As they do for other payment services, many banks may choose to maintain access to more than one instant payment service to attain resiliency through redundancy.”

Shared Standards

FedNow is expected to offer RFP and other competitive benefits, while supporting person-to-person payments not offered by RTP or ACH. Of particular interest to smaller banks may be a liquidity tool to help deal with cash-position surprises, Baumann said.

FedNow, RTP and ACH have in common adherence to the ISO 2022 messaging standard; the first two are built on versions of the Vocalink platform, owned by Mastercard, as are real-time payment services in other countries including Canada, Singapore, Sweden and the U.K.

TCH's Ledford said upwards of 50 countries have payment systems similar to RTP, an experience base that that TCH can learn from and build upon.

Baumann said the shared technical standard and similar technology could potentially facilitate network linkages to enable cross-border payments in real time.

On Blockchain

In an existing cross-border payment system, Ripple has hundreds of financial institutions in more than 80 countries using its blockchain solution. Mastercard and Visa have also developed blockchain-based services.

“Our current global financial system does not meet the needs of 1.7 billion unbanked people,” Ripple says on its website. “Digital assets and distributed ledger technology have the potential to transform how unbanked and underbanked populations access basic financial services and send and receive money across borders, making it more accessible, affordable and secure.”

“It may be hard to do business in some emerging regions of Africa, but through this technology it becomes much easier to reach them from a payment perspective,” Baumann noted.

For domestic payments, RTP-type networks tend to be faster and cheaper, depending in part on banks' pricing decisions. Transaction costs of cross-border payments via blockchain are 40% to 80% less than on traditional payment rails, according to Deloitte.