In response the pandemic, borrowers across Europe were given more time to repay their loans in 2020, with the help of government-support programs and guidelines issued by the European Banking Authority (EBA). But the moratoria in many European countries are drawing near to expiration, and there are now questions about how the expected phase-outs of the so-called “payment holidays” are not only going to impact debtors but also banks' credit risk.

Will borrowers, for example, have a difficult time repaying loans after the moratoria expire, and will we consequently see a significant spike in non-performing loans (NPLs) and defaults? Have banks already taken steps to account for potential loan losses from the moratoria, and how could the trends we're seeing affect expected credit loss projections under the IFRS 9 accounting standard?

A recent EBA report stated that, as of the end of June 2020, roughly $1 trillion worth of bank loans in Europe were granted moratoria. These “paused” loans comprised roughly 6% of banks' total loans and represented 7.5% of total loans issued to households and non-financial corporations (NFCs) in Europe. They were given, in part, to small- and medium-sized enterprises (16% under moratoria of total loans), commercial real estate (12%) and residential mortgages (7%).

For banks, one of the most revealing findings of the EBA study was the riskiness of moratoria loans. The regulator found that 17% of loans under moratoria are categorized as “stage 2” under IFRS 9, and hence carry a higher risk of defaulting.

What remains somewhat unclear is when, exactly, the loans on payment holidays across Europe will expire. In its report, the EBA said that 85% of these loans were scheduled to be phased out before this month - but also stated that “some countries” have already extended payment freezes.

Whenever the moratoria expire, if borrowers don't repay their loans, banks could face serious issues with the build-up of huge debt down the line. To avoid placing their loan books in jeopardy, banks are, in fact, preparing for significant losses resulting from debt writeoffs. Indeed, a November Reuters report stated that 10 large European banks have already allocated €45 billion to the cost of unpaid loans.

Findings of the EBA's Investigation

Many banks have a good chunk of their loans tied up in payment holidays, according to the EBA's report. Distressed debt, consequently, is on the rise in Europe.

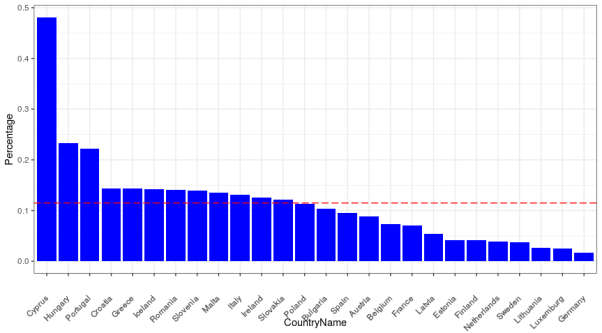

While noting that COVID‐19‐related moratoria have provided “breathing space” to borrowers, the EBA noted that loans under moratoria represented a significant percentage of all European loans. In many countries, banks reported that more than 10 percent of their total loans are under moratoria, and in some countries (e.g. Cyprus, Hungary, Portugal) that number is higher than 20%.

The figure below (a reproduction of an EBA visualization) depicts loans under moratoria for households and NFCs; the red dotted line is the unweighted average.

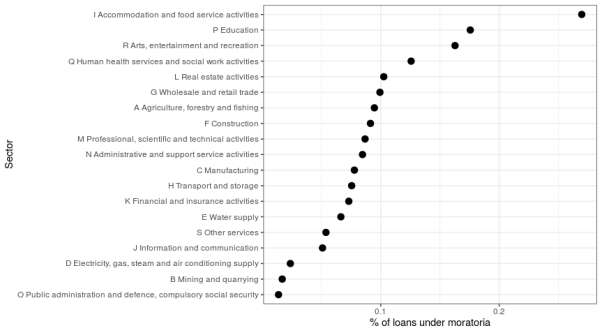

Not surprisingly, the sectors most affected by the moratoria include restaurants, bars, education, entertainment and recreation - i.e., everything that makes life worth living but cannot be enjoyed under a social distancing or lockdown regime.

Cliff-Edge Effects

Without government support, might we see a wave of loan defaults? The EBA describes this scenario as one of the “cliff-edge” risks of a phase-out of the moratoria. If this were to happen, we could potentially see a sudden and significant increase in the level of NPLs.

The expiry of the moratoria could make for a dangerous mix with, say, a prolonged economic downturn. On the other hand, as the EBA notes, extensions of the moratoria could have a negative side effect: the development of a “non-paying” culture among borrowers. Indeed, when borrowers start taking government guarantees for granted, payment holidays can, in some cases, be a dangerous treatment.

Parting Thoughts

The upcoming months will be crucial for banks' IFRS 9 expected credit loss calculations. In some cases, banks will see that the previously established relationships between macro-economic variables and probability of default (PD) will break down: e.g., thanks to the moratoria, a decline in GDP will not necessarily be reflected in arrears and default statistics.

Regardless of whether the moratoria are extended or phased out, it will be far from easy to interpret the current state of the market. Indeed, it will be very difficult to “read” the 2020 outcomes and derive any predictive power from them. Projecting IFRS 9 credit losses for next year and beyond could therefore prove quite challenging.

Dr. Marco Folpmers (FRM) is a partner for Financial Risk Management at Deloitte Netherlands. He is also a professor of financial risk management at Tilburg University/TIAS.