As a general rule, the bigger the bank, the more sophisticated its credit-risk models. But determining the size of a bank is very dependent on one's measurement approach. The same holds true, on a micro level, for calculating a bank's largest portfolios.

Every November, the Financial Stability Board publishes the list of global systemically important banks (G-SIBs), allocating the largest banks into five groups. G-SIBs must hold extra capital, but the exact amount is dependent on the group to which a bank is assigned. Group 5 banks, for example, have to have an additional buffer (“GSIB buffer”) of 3.5%, while the G-SIB buffer for Group 1 is 1%.

We'll soon learn the identity of the FSB's 2021 G-SIBs list. Last November, Citigroup, HSBC and JPMorgan Chase (group 3) - and Bank of America, Bank of China, Barclays, BNP Paribas, China Construction Bank, Deutsche Bank, Industrial and Commercial Bank of China, and MUFG (group 2) - were among the world's largest banks.

For each G-SIB, the FSB determines an overall score, with the help of a Basel Committee methodology. The Basel Committee calculates scores on each of the following five indicators: size (total exposure, as determined for the calculation of the leverage ratio); cross-jurisdictional activity; interconnectedness; substitutability; and complexity. Further details and definitions can be gathered from the BIS site.

What's the Largest Bank?

Each year, the FSB calculates the extent to which banks are affected by the five attributes listed above. The overall score for a bank is simply the unweighted average of its scores for the five attributes. “The methodology gives an equal weight of 20% to each of the five categories of systemic importance,” the Basel Committee explains.

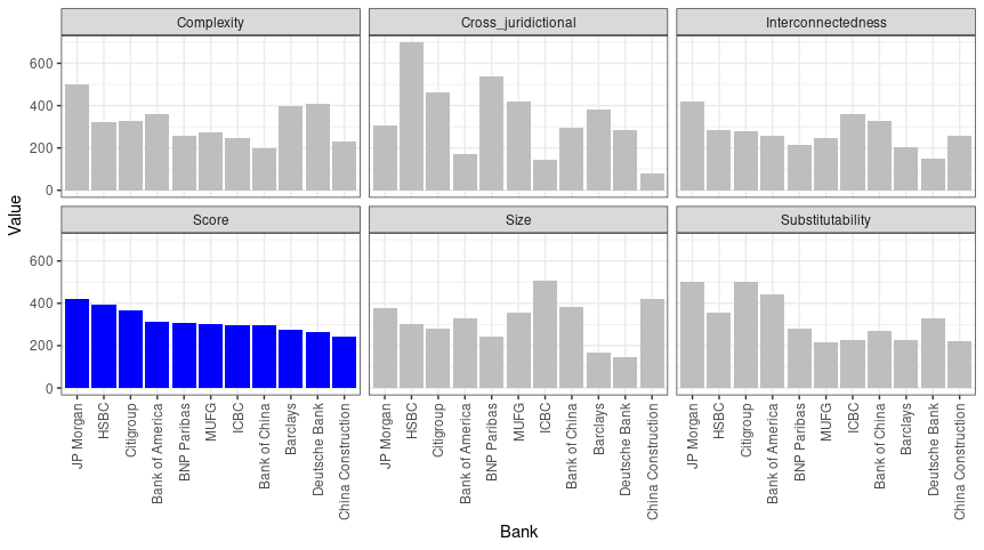

In the chart below, we show the FSB's 2020 scores of the banks in the two largest G-SIB groups (groups 2 and 3) - both for the five attributes (in grey) and the overall score (in blue).

Overall Score and Constituent Scores for G-SIBs

When analyzing the above data, it becomes immediately apparent how much “the largest bank” is a subjective opinion, rather than a fact. If the Basel Committee would only slightly update its methodology (e.g., by omitting one attribute or by adding a different weighting scheme), the G-SIB landscape would look entirely different.

Model Tiering

Measuring size is not only relevant at the macro level - it also helps banks identify and understand their largest portfolios. Leveraging this data, moreover, banks can set priorities on an impact basis, using more sophisticated models wherever there is more risk.

If there are two trends that have emerged from the past 20 years of credit risk and capital modeling (taking the Basel II accord as a starting point), it's the increasing complexity of approaches and the growth of the model landscape. This growth has been supplemented by an ocean of model code, documentation and validation reports that are sometimes overwhelming.

One of the countermeasures to deal with this increasing information overload is tiering. Model tiering occurs when the credit portfolios of the bank are categorized along their significance - e.g., in classes A, B, C and D. A fundamental assessment of the model landscape tends to be a long-term and delicate activity, but intermediate results can be booked by setting up an appropriate model tiering.

With the help of model tiering, a bank can prioritize its models based on materiality. Subsequently, model development and validation efforts can be planned in such a way that more effort is spent on material models, rather than on models that are applied to insignificant portfolios.

One can question whether model tiering should be based on total assets (or similar measures, like total EAD) or risk-weighted assets. There's something to say for both.

Models are easier initiated than discarded; consequently, there is an organic trend toward more models. This has led to an increased model workload for a limited range of available experts. Model tiering can help resolve this issue, but it's not the only solution.

The fundamental approach is, of course, looking at the model landscape itself. There's a continuous pressure for banks to look for better model performance, higher granularity and new models for new portfolios. But fundamental questions should still be asked about the relevance of each model, and critical assessments of their value are needed to deter the development of unnecessary methodologies.

Parting Thoughts

Model tiering is one of the most important tools for model risk management, and evidence shows that most banks use it to allocate models to priority classes. Interestingly, the calibration of model-risk tiering tools is largely judgmental.

The same is true on a macro level, particularly when we consider the factors that are used to determine the world's largest bank. Data, effective models and, above all, judgment are required.

Dr. Marco Folpmers (FRM) is a partner for Financial Risk Management at Deloitte Netherlands.