“The future is not set,” said Kyle Reese, the hero in The Terminator movie. That, believe it or not, may turn out to be the most valuable lesson COVID-19 has taught the risk community and business managers: i.e., since there are many possible futures, it clearly isn't enough to look at - and prepare for - just a few of them.

To prepare for the unexpected and the unprecedented, one needs a full suite of scenarios. But the multiple-scenarios strategy presents its own challenges.

First, it's difficult to estimate your credit allowance, capital and liquidity for even a single stress scenario. Essentially, this means that you have to apply a hybrid modeling approach - one that combines the best of technology innovation (like AI) with human judgment - to multiple scenarios.

Second, it is no easy task to decide which scenarios to use to be prepared for all potential events. Scenarios, however, come with their own probabilities (in their full distribution), so it's possible to prepare for highly-probable scenarios while watching out for less probable - but more severe - ones.

Think of it this way: how should you prepare yourself for a potential fire in your house? You wouldn't call in fire fighters “just in case.” Rather, you'd buy fire insurance and install smoke detectors. Under such an approach, you can live a normal life while simultaneously being prepared for a fiery outcome.

This is exactly how scenarios can be used: to establish early warning signals and contingent actions.

Early Warnings Through Dynamic Correlations

There are two extreme courses of action with respect to future uncertainty: reactive (i.e., acting after the fact) and overly conservative (i.e., having provisions that cover even very unlikely scenarios). Neither of these is suitable for a bank.

Reacting to a crisis as it unfolds is bound to be inefficient. Deciding on a course of action takes time, and the fact that the situation is likely to keep deteriorating only complicates the matter.

Conversely, stocking up provisions for a one-in-a-thousand-year scenario is also not feasible solution. In fact, the overly-conservative approach might put a financial institution at a disadvantage relative to competitors with a more aggressive risk appetite.

The optimal course of action that lies between these extremes is a multiple, dynamically-generated scenario approach, because it provides a platform for identifying early warning signals.

Such signals are based on correlations between a particular objective and other variables. (For example, a major economic shock would simultaneously push credit spreads up and equity prices down.) To make it possible to pinpoint where on the probability distribution they occur, these signals must be dynamic.

Scenario generation must create a realistic impact of potential shocks and the knock-on effects they can cause. Only then can the full distribution of final outcomes show hidden, implicit correlations with the underlying drivers of these outcomes.

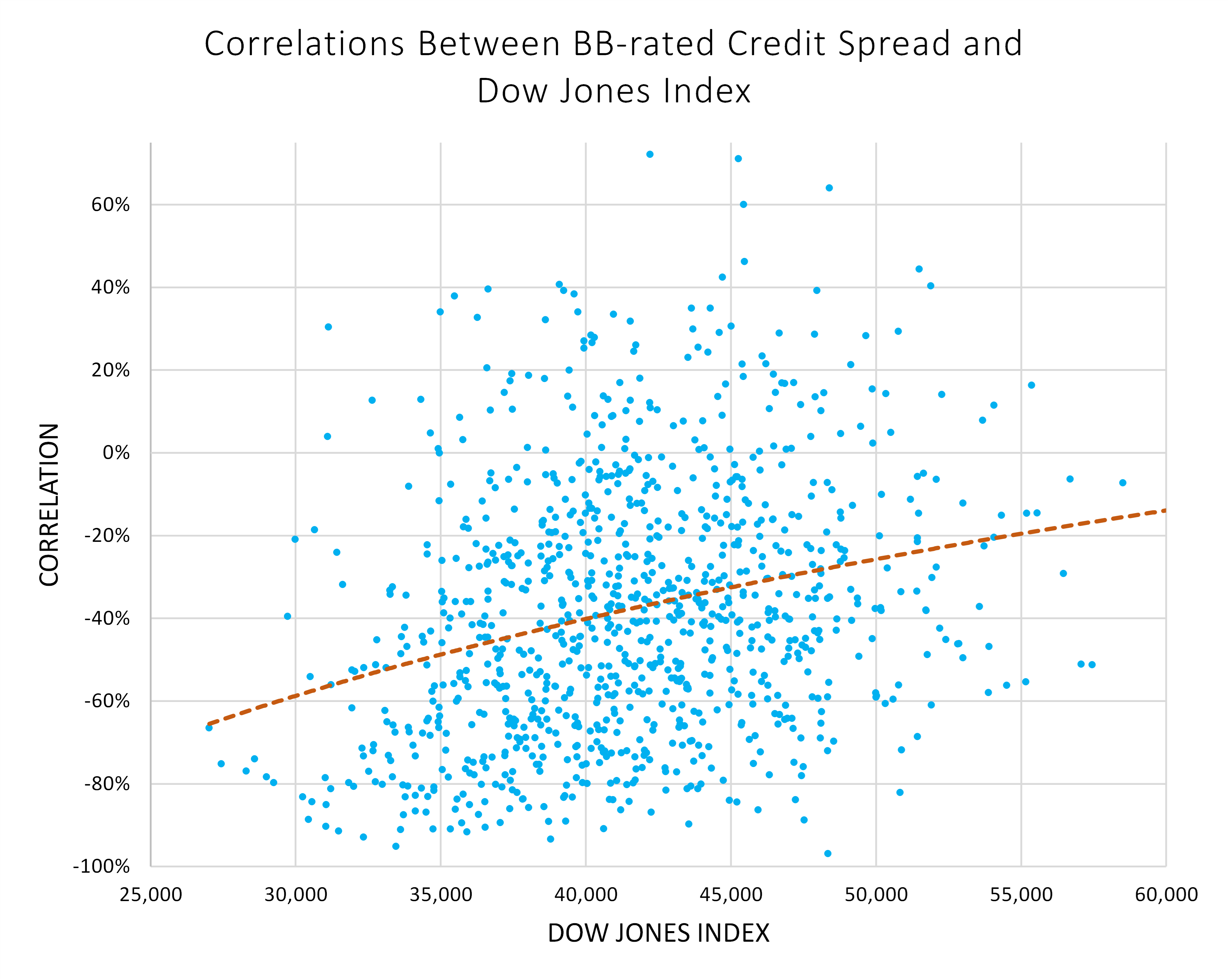

In response to a major shock, the implied correlation between credit spreads and equity markets will be different from the historical one (see Figure 1).

Figure 1: Dynamic Correlations Between the Credit Spreads and Equity Markets

Above, we calculated the implied correlations along simulated paths. You can see from this chart that when the average level of the Dow Jones index along the path is falling, its correlation with the credit spread is getting more negative.

Through this dynamic approach to scenario generation, you get different implied correlations in different parts of the distribution. This gives you an opportunity to identify early warning signals, as you can see which variables are highly correlated with the specific outcomes in which you are interested.

Signal Identification

To illustrate how you can recognize these signals, let's consider the key performance indicator (KPI) outcomes in a particular percentile. All scenarios leading to these outcomes will form a very narrow cone, as the values, by design, must be close. Any other variable that also forms a narrow cone on exactly the same scenarios might be considered an early warning, since it's correlated with that particular outcome.

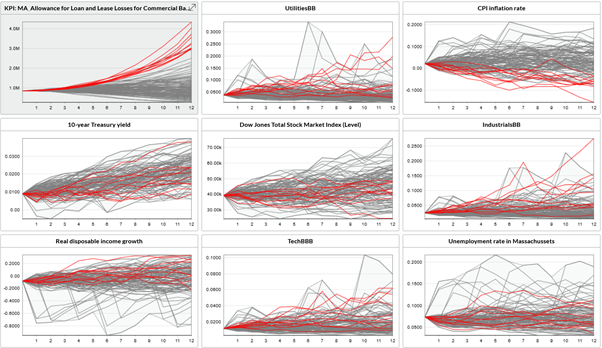

In the example below (Figure 2), every plot represents consistently-generated variables (a thousand of them), shown by the gray lines. The red lines, on the other hand, identify the worst 10 paths of the aggregated allowance for loan and lease losses (ALLL) for a certain type of bank. They are the same scenarios highlighted in all plots.

Figure 2: Scenario Variables on the Paths Where Allowance Is Very High

In some of the plots in Figure 2, the red lines completely cross over the gray ones. These are the variables that cannot serve as early warning indicators, because they are not correlated with the worst-case ALLL outcome that was selected as the most critical KPI.

There are, in contrast, plots (like CPI inflation) where the red lines are clustered together. These are the variables that can be used as early warning indicators.

Obviously, the charts can give you only an intuitive impression. Given the full distribution of all underlying variables (with their consistent behavior in all scenarios), one can use clustering techniques to automatically identify which variables are highly correlated with a particular KPI's outcome.

You could, for example, identify variables that correlate to the baseline or optimistic outcome - or to something more specific, like the worst-case or 75th percentile of capital, liquidity or earnings distribution.

Most importantly, you can do this only when you have scenarios with dynamic correlations. Static multidimensional distributions and traditional regression methods will only show you historical dependencies.

Some of these dynamic correlations can be anticipated; in a crisis, for instance, a country's credit spreads have a higher correlation with the respective exchange rate than during stable periods. Others will be less obvious - like, say, a slightly-humped yield curve leading to negative earnings because of a mismatch of embedded optionality on the asset and liability sides.

In either case, analysis of dynamic correlations will either verify and support the risk identification process or show what else should be included.

Forewarned Means Forearmed

Senior management of financial institutions can use early warning signals to avoid the pitfalls of acting too late or too soon.

Of course, you cannot time the market. But let's say you observe that the probability of an adverse outcome has increased from 0.1% to 5%, and that early warning indicators have crossed some boundaries established in your risk identification process. Under this scenario, having the proper triggers in place will help senior management activate contingency plans.

Since they take a long time to develop, such plans must be established far in advance. And here, again, is where the advantage of multiple scenarios comes into play.

When an organization has identified the range of undesirable values for their KPIs - what balance sheet composition causes them, and what macroeconomic and market conditions (i.e., scenarios) lead to them - it can work on a mitigation plan. Potential solutions (e.g., balance-sheet modifications, strategic hedges, adjustment of risk limits or funding) must then be overlaid over all scenarios, to make sure they don't inadvertently create another hidden pocket of risk.

Parting Thoughts

The methodology described in this article can be used not just for stress testing but also for optimal balance-sheet strategies.

Since it identifies early warning indicators for idiosyncratic KPIs, this multi-pronged scenario approach can help financial institutions avoid systemic risk. Institutions using this approach should have in place specific trigger variables and levels, as well as contingency plans based on these triggers.

Alla Gil is co-founder and CEO of Straterix, which provides unique scenario tools for strategic planning and risk management. Prior to forming Straterix, Gil was the global head of Strategic Advisory at Goldman Sachs, Citigroup and Nomura, where she advised financial institutions and corporations on stress testing, economic capital, ALM, long-term risk projections and optimal capital allocation.