Menu

Modeling Risk

Friday, March 8, 2019

By Tony Hughes

Stress testing, up until now, has basically been a theoretical exercise. Growth has been slow but steady and the imbalances that can trigger recessions have largely been absent. However, with many now calling for a 2020 U.S. recession - and with Brexit looming - we may soon find out whether stress tests actually work when applied in the real world.

With these developments in mind, bankers are steeling their nerves and taking a keener interest in what their credit loss models are currently telling them. Most models are trained on data from the Great Recession, but the next event looks like it will be a horse of a rather different color. The condition of the banking system in 2019 is also quite distinct from that which existed back in 2007, on the eve of the last major economic crisis.

Given these realities, it is prudent to consider the state of the industry and identify products that may be especially vulnerable given the nature of the anticipated recession. Under this lens, one asset class stands out: commercial lending.

While the 2008/09 downturn was caused by excesses in consumer lending, the hypothetical 2020 recession may well be driven by trade frictions that will impact the commercial sector head-on. Consumer loans, stung by their terrible performance during the last recession, are now likely to play second fiddle.

Commercial loans have generally exhibited historical recession behavior that is product-specific. During the 2001 recession, commercial and industrial (C&I) lending suffered disproportionately high losses while commercial real estate (CRE) was barely touched. This was because the immediately preceding dot-com boom brought with it high levels of risky C&I lending.

Conversely, the CRE industry at the time - cognizant of the burns it had sustained during the disastrous 1990 recession - steered clear of all major heat sources through much of the subsequent decade. The Great Recession did see high loss rates in both products, but this result was due primarily to the depth of the downturn.

CRE Risks

The concept of a “hot” market is highly pertinent in determining which lending products are most at risk. If a particular product has experienced a long period of above-average growth, it is likely that lenders relaxed their normal standards to prolong it. A hot market is not a necessary condition for a product to experience recession-era problems, though it is often a sufficient one.

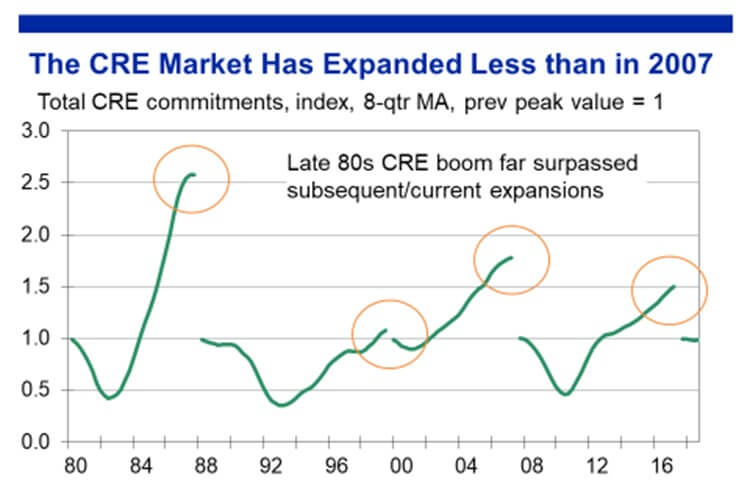

Figure 1: Commercial Real Estate Expansion Rates

Though heat is largely absent in the CRE market at present, many models are suggesting high potential losses in the looming recession. This is a recognition of the fact that the quality of underwriting, in addition to its scope, is a key determinant of recession-era performance for all products.

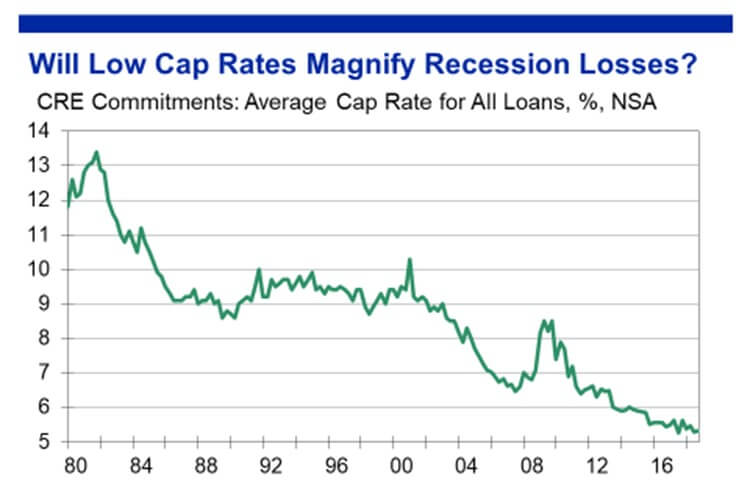

The startling feature of the CRE market at present is that cap rates - net operating income divided by the market value of collateral - are rapidly declining and are already at an all-time low. (See Figure 2, below). The CRE market has never entered a recession where income generation had been so poor relative to property valuation during the preceding expansion.

Figure 2: The Steep Fall of CRE Cap Rates

Declining cap rates are strongly associated with higher rates of default in loan-level CRE models. It is unclear how ultra-low cap rates interact with the broader economic cycle, since we are now well outside the domain of historical recession-era data. CRE lenders may have erred in choosing to extend credit in the context of such low cap rates; risk modelers are right to be cautious in making pessimistic stress projections in the current environment.

Leveraged Lending Vulnerabilities

The area with the most heat in the commercial sector is leveraged loans. Growth in these assets has been global in nature and was spectacular right up until 2017. Some have likened this trend to the rise of subprime mortgages in the mid-2000s.

The nature of leveraged loans is that they are made to riskier corporations, generally with weak or non-existent loan covenants in place to protect lenders. Once originated, they are either held on the balance sheet of banks or packaged into collateralized loan obligations and sold to other investors, sometimes including other banks. Leveraged-loan growth slowed in 2018, suggesting some amelioration of risk, though this may be cold comfort for those already holding large exposures.

Given the risky nature of leveraged loans, the sector could be vulnerable to a recession centered on the commercial sectors of the economy. With that said, adjectives can sometimes be misleading - just because a borrower is “leveraged” or “subprime” does not necessarily imply certain doom. But not diligently underwriting these adjective-laden borrowers generally does.

The corporate-lending landscape is a diverse place; apart from the rise in leveraged lending, the C&I market appears to be well balanced. The industry suffered from the effects of a mini-recession in 2016 that mainly affected oil and gas producers. That event caused lenders to tighten underwriting standards and slow the rate of new loan origination.

Parting Thoughts

If the 2020 recession comes to fruition, commercial lenders may view the minor difficulties of 2016 positively, since they acted as a release valve, improving the state of the industry's books on the eve of more troubling times.

So, for those looking for potential recession crises in the banking sector, low CRE cap rates and the extraordinary rise of leveraged lending appear to be the most likely contenders.

Here's hoping that the next recession is short, mild or non-existent. As a stress tester, not knowing whether your efforts will make any difference is the best possible situation.

Tony Hughes is a managing director of economic research and credit analytics at Moody's Analytics. His work over the past 15 years has spanned the world of financial risk modeling, from corporate and retail exposures to deposits and revenues. He has also engaged in forecasting of asset prices and general macroeconomic analysis.

Advertisement

•Bylaws •Code of Conduct •Privacy Notice •Terms of Use © 2024 Global Association of Risk Professionals

More

More