Menu

Risk Weighted

Friday, June 26, 2020

By Tony Hughes

Modeling climate risk, and analyzing your risk of default, is extremely difficult - particularly if you are an electricity provider. All one has to do to realize the enormity of this challenge, and the potential havoc climate change can wreak on a business' bottom line, is to consider recent events on either side of the Pacific.

I am Australian by birth and sporting allegiance. Immediately prior to the COVID-19 outbreak, the worst bushfire season in the living memory of my homeland came to dominate the world's headlines. Wildfires have always been a fact of life for the Sunburnt Country, but this was something altogether different. The last decade, and especially the last year, have been off the charts in terms of the scale and intensity of Australian fires.

The news from Down Under can be interlaced with the ongoing bankruptcy of Pacific Gas and Electric (PG&E), considered to be the largest climate-related business failure in history. This Californian utility was forced into bankruptcy by legal settlements stemming from the deadly 2018 Camp Fire, which was literally sparked by faulty PG&E equipment. To anyone currently following the PG&E saga, the largest class-action lawsuit in Australian history - brought against an electrical utility that caused a devastating 2009 bushfire - would be eerily familiar.

Electricity providers are well aware of the costs associated with service provision in dry, remote areas that are heavily forested. When fire risks and capped prices are laid on top of high maintenance costs, one suspects that risk-adjusted returns for these regions fall to a point that is well below breakeven. Utilities like PG&E still provide services in these regions because they are required to do so by regulators, with city folk providing the profits that subsidize their remote-living compatriots.

The value of the PG&E franchise was clearly affected by climate change. With 2020 hindsight, pre-2018 managers would have negotiated - and regulators would have agreed to - a deal like the one currently under discussion in California. This arrangement includes $20 billion to cover costs of future wildfires, increased allowance for maintenance costs in remote areas and proscribed rules allowing providers to shut off power to locations facing extreme weather conditions. A deal like this recognizes that some wildfire risks are no longer insurable in the private sector, requiring some level of state intervention to ensure continuing service in remote areas.

California and Australia share the common myth of being rugged frontier lands; in reality, the majority of people live in modern, well-serviced urban or suburban districts. The myth, however, creates a strong political will to support people who still choose to live out on the edge of civilization.

I suspect that PG&E's failure was primarily caused by the interplay between the willingness of its regulators (e.g., the California Public Utilities Commission and the Federal Energy Regulatory Commission) to buttress the market, the company's need to earn profits for their shareholders and the cold reality of global warming. For PG&E to have survived the 2018 fire season, the company and regulators would have had to agree on a deal that no-one knew was needed.

Quantifying Climate Credit Risk

The lessons for investors and creditors in regulated corporate entities are fairly clear. The industry, though, is hungry for more generalized clues about how climate risk can be quantified.

Such models should be able to provide the following information: if the climate had remained like it was in, say, 1980, Company X would have an estimated one-year probability of default (PD) of 2% right now. Given today's climate reality, holding all else equal, the PD would be estimated to be 5%. If there had been an additional degree of warming by now, the company's default likelihood would be expected to rise to 10% under present day baseline economic conditions.

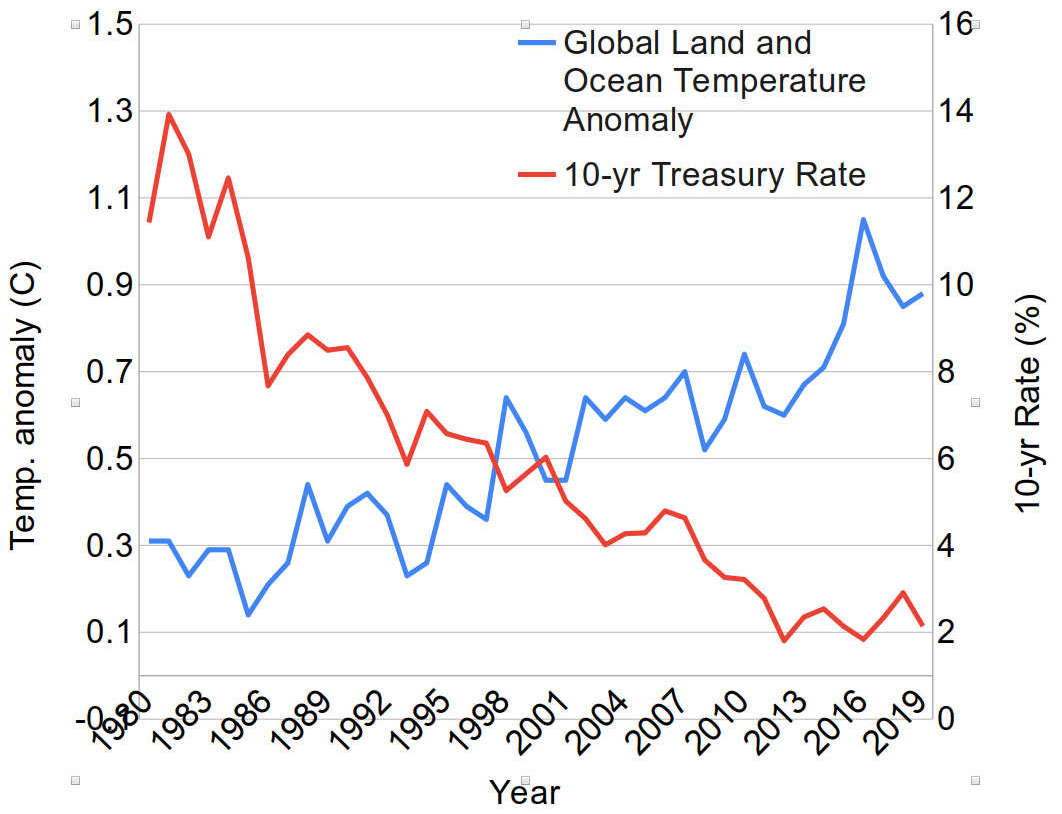

To highlight how difficult this modeling task is, we can look at trend data over the past 40 years. While global temperature anomalies have trended ever higher since 1980, various critical economic factors have also exhibited strong trend behavior. To cite one example, U.S. long-term interest rates declined almost inexorably (from around 14% to 2%) over this 40-year period, which corresponds precisely to Chairman Volcker's efforts to defeat inflation and the subsequent Great Moderation.

Temperature and Interest Rate Trends, 1980 - 2020

To separately identify the climate sensitivity of different credit exposures, we will need to rely far more on cross-sectional variation than is typical in other stress testing applications.

Arriving at the desired output with such data, though, is very tricky. We need to scale regions around the world by climate risk and then infer, for example, that Northern California plus one degree of global warming has equivalent fire risk to Southeastern Australia today. Many climate risk datasets on the market at present are highly granular and clearly up to this task.

We then need to tie the climate back to financial data and defaults.

Challenges and Lessons

A company will be at high risk of climate-related default if it has critical assets concentrated in climate-sensitive areas that cannot easily be insured or relocated. These assets may be tangible or intangible. A widget-maker, for instance, may be unable to insure a building that it subsequently loses to wildfire; a service provider may lose years of local customer loyalty and goodwill if its home region is devastated by a natural disaster.

In PG&E's case, its business was all about providing electricity to Californian businesses and households, regardless of the weather. One lesson from its failure, therefore, is that we must be cognizant of geographical concentrations and the mobility of critical assets on corporate balance sheets.

Make no bones about it, modeling the impact of climate on financial interests will be extremely challenging. Under such circumstances, there is often a strong motivation for risk analysts to forego rigor and rely instead on subjective assessments and management overlay.

In a field where the value of scientific endeavor itself has been questioned, it is especially critical that a data-driven solution to the problem of climate stress testing be found.

Tony Hughes is a risk modeler and economist. He is a credit risk analytics expert and thought leader with many years of experience building high-caliber risk modeling and data science teams.

•Bylaws •Code of Conduct •Privacy Notice •Terms of Use © 2024 Global Association of Risk Professionals

More

More