Menu

Modeling Risk

Friday, April 5, 2019

By Tony Hughes

Smaller lending institutions face a dilemma. The primary motivation behind the Current Expected Credit Loss (CECL) standard is to provide investors with enhanced forward-looking information about the state of the lending book. Producing high-quality/ low-volatility forward estimates, however, is difficult and can be expensive.

Moreover, if the new accounting methods achieve their stated aim, there is a danger that a technological gulf will open between large banks and their smaller brethren.

We have already seen some big IFRS 9 banks operating outside the US release annual reports under the new protocols, and the results have been impressive. Most banks have disclosed detailed comparisons that show the losses that might be expected under multiple economic scenarios and under different assumptions regarding the staging of loans. Investors can use this information to gauge their potential exposure if external conditions go haywire, or if bad loans start to be revealed.

If smaller institutions fudge these questions, investors will have a far dimmer view of the financial positions of the banks in question. Small lenders already face higher funding costs than larger ones; the technological gulf likely to be created by CECL can only act to magnify this gap.

Just Say No to WARM

Against this backdrop, community banks in the US are grappling with the question of CECL implementation. They won't have to worry about modeling the staging mechanism under the US version of expected loss accounting, but they still need to satisfy their investors with detailed information that at least approaches the quality of large-bank disclosures.

Recently, there has been a lot of discussion about weighted average remaining maturity (WARM) as a potential solution to this problem. The Financial Accounting Standards Board (FASB), for its part, sparked interest in WARM via a January Q&A that seemed to greenlight the method for CECL adoption.

However, this method is not forward looking in the sense that it applies observed historical loss rates to the remaining contractual term of loans on book, adjusted for the probability of prepayment. These loss estimates are adjusted subjectively to account for potential changes in the economic outlook.

The problem with WARM is that it is a terrible way to gauge future losses. A recent study considered a number of different modeling approaches for CECL and concluded that WARM was perhaps the worst, flatly warning that “WARM should not be used for CECL.” The American Bankers Association echoed this view in a January paper, opining that institutions need to “seriously reconsider” whether WARM is appropriate for their organization.

Despite these admonitions, many community banks are still seriously considering WARM as their sole CECL strategy. This may be a valid de minimis approach, but we think small banks can do a better job.

WARM is normally implemented using call reports. This database is a complete record of the financial behavior of banks, both active and defunct, going back to the early 1990s. It is freely available on the Federal Deposit Insurance Corporation website.

Critically, the database includes gross and net credit losses and outstanding volumes for 14 different loan categories. Viewed objectively, call report data is a treasure trove of information about past bank financial performance. An equivalent database is available for all US credit unions and in a handful of other countries.

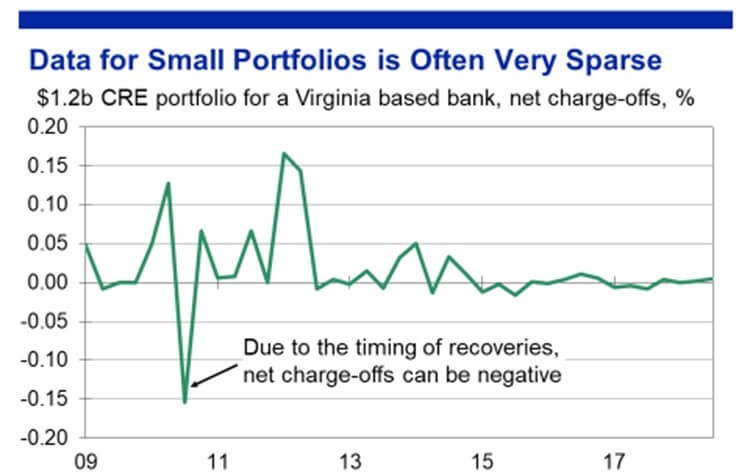

While you can model call report data, you must be careful. Data on small portfolios tends to be inherently sparse. A $1 billion bank with a commercial portfolio may go quarters or even years with zero defaults, and then, usually during a recession, experience a cluster of local business failures that cause losses to spike dramatically.

Let's take a look at the CRE portfolio of an actual bank based in Virginia. This bank has a sizeable $1.2 billion portfolio, but its credit loss history is very sporadic (see Figure 1). At first glance, you'll see that loss spikes at this bank were larger and more frequent in 2009 and 2010 than they were in 2017 and 2018. It would be extremely difficult to model and forecast this choppy data with any degree of accuracy.

Figure 1: CRE Portfolio Example

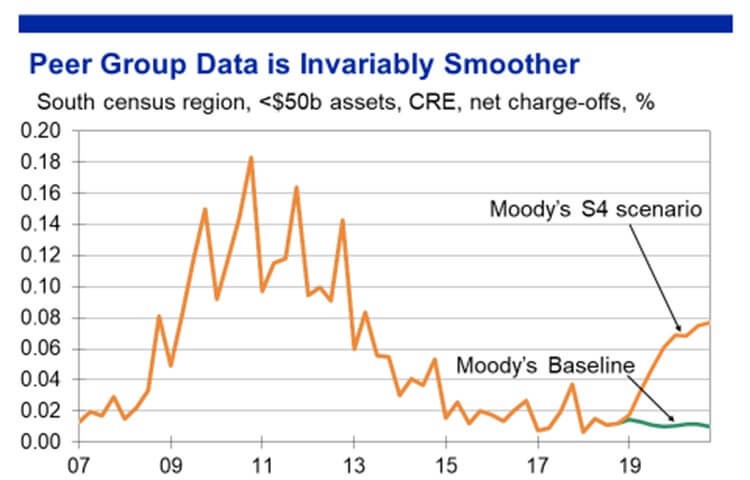

The Peer Data Panacea

The solution to this problem is to find more data! There are around 5,000 banks in the US (most of them small) and approximately as many credit unions. Among these institutions, it is possible to define peer groups whose aggregate risk appetite approximates that of the target bank. The data for this cluster of banks will be far smoother, thanks to the law of large numbers, and thus conducive to the construction of more accurate and stable baseline and stress projections.

For our sample bank, we can form a peer group of all banks with under $50 billion in assets located (like our bank) in the South census region. This data is far more manageable, and we can proceed to relate the series to economic drivers and build forecasts and stressed economic scenarios (see Figure 2).

Figure 2: Peer Data for Banks in the South Census Region

We can then make assumptions regarding the reasonable and supportable forecast period, and derive relevant CECL reserves numbers for the bank's portfolio. Using an eight-quarter period, we find that our sample bank should reserve $898,000 for Q1 2019 under a baseline projection and $3.81 million under the severe S4 (protracted slump) recession scenario.

The puny baseline figure reflects the fact that CRE losses are typically very low - the odd basis point or two - in an expanding economy. This result thus highlights the importance of using stress scenarios in developing CECL numbers. Fears of a 2020 recession abound, and loss provisions will be far too low if the WARM method is applied to this portfolio (losses in recent years have been effectively zero) or if baseline projections are used in isolation.

If we were to conduct a full risk management analysis for our sample bank, we would of course define the peer group more carefully, or triangulate using a range of potential peer groups.

The moral of the story is that good-quality CECL projections can be developed using high-quality data that is available free of charge. Even the smallest bank with the sparsest default history can identify a set of peers reflective of its own portfolio. In disclosure, these banks could report multiple peer group comparisons and satisfy investors that they are sufficiently reserved.

It is not true that small banks have no options. Loss modeling may be challenging, but it does not need to be expensive.

Tony Hughes is a managing director of economic research and credit analytics at Moody's Analytics. His work over the past 15 years has spanned the world of financial risk modeling, from corporate and retail exposures to deposits and revenues. He has also engaged in forecasting of asset prices and general macroeconomic analysis.

Advertisement

•Bylaws •Code of Conduct •Privacy Notice •Terms of Use © 2024 Global Association of Risk Professionals

More

More